The real wage gap once again

Miguel Lebre de Freitas, 4-12-2013

Intro

It is amazing how wrong ideas can last for

so long, just because they fit well in the narrative: it became vox pop that wages

in Portugal have increased ahead of productivity, eroding external

competitiveness, and that this caused the huge current account deficits that

emerged in the decade before 2008. Fortunately, along the last couple of years,

the profession has increasingly recognized the role of capital flows as the

main drivers of external imbalances across the euro area. Still, the claim that

wage-setting institutions in Portugal are naïve and eventually not prepared to

live in a low inflation environment remains very popular in the opinion-making

arena and is feeding speeches of radical euro-sceptics.

As I already argued here (and here),

the evidence does not conform well to the idea that the private sector in Portugal

engages in crazy wage setting. However, my purpose at that time was to explain

why economy-wide indexes of relative unit labour costs are poor measures of external

competitiveness. In this post, I use the available data more intensively, to refute

the claim that wages have increased above productivity. Actually, as for the

last couple of years, the data suggests exactly the opposite: real wages look

like having fallen below the productivity trend. This suggests that, if private investment

is not responding at this moment, the reason should not be labour costs, but something

else.

The variables used

Before starting, allow me a little remark:

the following discussion presumes that the elasticity of substitution between

labour and other inputs in the production function is equal to one. This is not

a general case, but it works well with the historical data and it looks like working

pretty well in the Portuguese case too - as we will see in a minute. But if you

don’t buy this, please stop reading here.

Now, let me introduce the four variables we

are going to play with. These are:

W - Nominal compensation per employee

(euros);

V – Gross Value added at constant prices;

L – Employment (1000 persons);

P – Price deflator of Gross Value Added.

The raw data are from the European

Commission, AMECO, backed by INE. The figure for 2012 has to be taken with

caution, as it is based on an EC forecast that comes ahead of the INE’ official

release.

The following sections explore different

combinations of these four variables. We focus on two broad sectors that

account for 80% of employment in Portugal: “Services” and “Manufactures”. It is

worth distinguishing these two sectors, because they are differently exposed to

international competition: manufactures consist on tradable goods only, while

services include both tradable and non-tradable. Moreover, in the case of

services, 1/3 of employment is accounted for by civil servants.

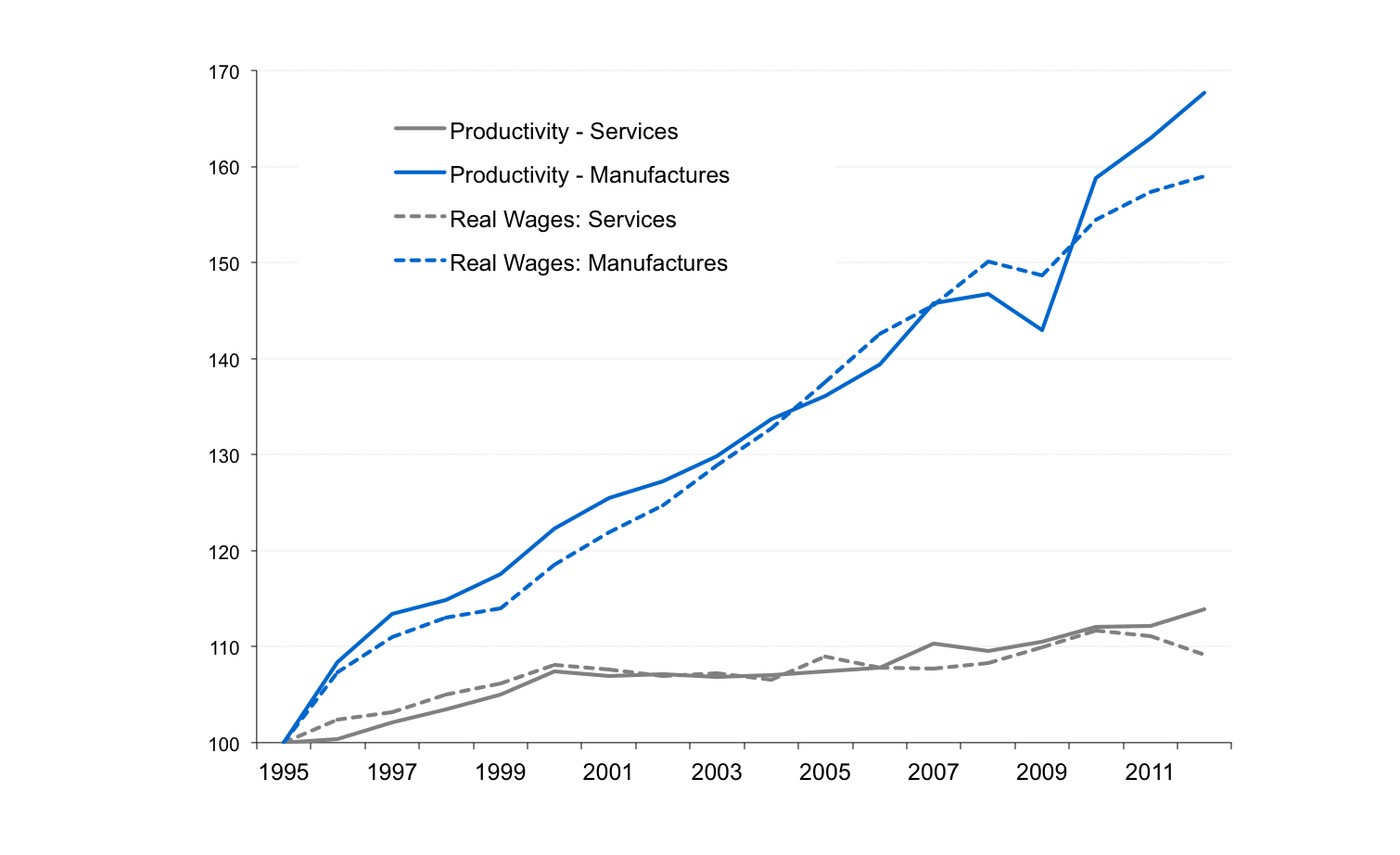

Angle 1: Real wages and productivity

We start with Figure 1. This figure

compares the evolution of real wages (W/P) and of the average product of labour (V/L)

in manufactures and in services, taking 1995 as the base year.

Figure 1: GVA per

person employed and Real compensation per employee (1995=100)

The first message in the figure is that productivity

growth has been much faster in manufactures than in services. This fact fits

well in the story that large capital inflows, by inducing a reallocation of labour

towards non-tradable goods, reduces a country’ exposure to the benefits of

learning-by-doing, delivering lower growth and long-lasting effects. In the case of Portugal, this adds to a productivity growth in manufactures that does not stand out in international terms.

The second message is that the indexes of real

wages and of productivity have evolved mostly in parallel. Interesting enough, during

the collapse of international trade in 2009, the productivity index in

manufactures fell more than that of real wages, but in the years that followed the

increase in real wages was smoothed downwards: it looks like inter-temporal trade

between workers and firms is taking place, as an informal insurance against

dismissals. In the case of services, the data in Figure 1 also points to a deceleration of

real wages relative to productivity during the bailout period.

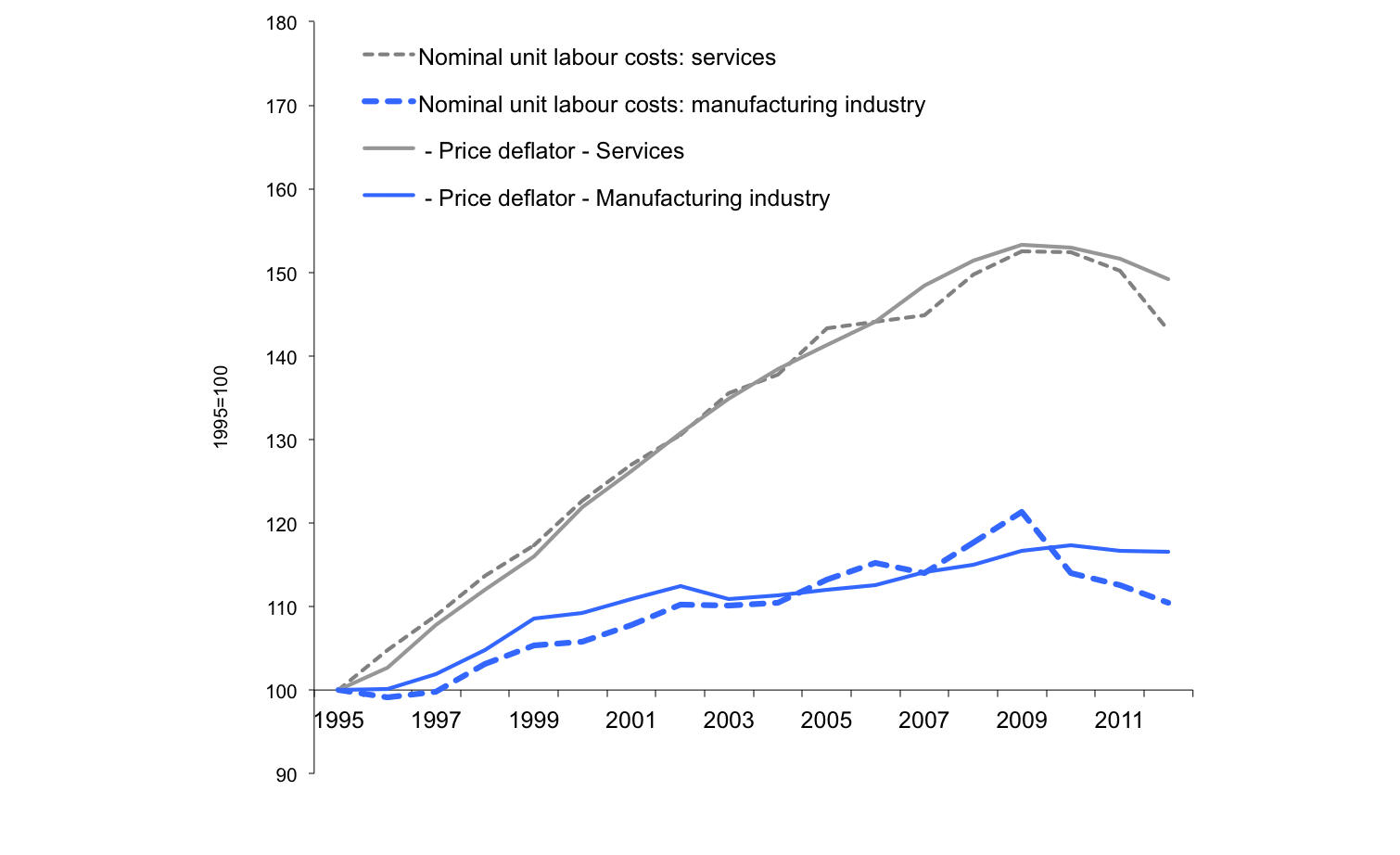

Now, we use the very same variables to

analyse the change in Unit Labour Costs, ULC=WL/V. In a world without frictions,

one should have P=ULC/b, where b denotes for the elasticity of labour

in the production function. In the case of tradable goods the output price is

determined abroad, so the gaps between unit labour costs and

prices can be taken as an index of external competitiveness (the famous Z in

Blanchard).

In Figure 2, we compare the indexes of Unit

Labour Costs and of Prices in manufactures and in services, using 1995 as the base year.

The first fact in Figure 2 is that unit labour costs in each sector remained close to price developments. Just like in Figure 1, in the case of manufactures we see a significant jump in ULC ahead of prices in the year of 2009, but this move was immediately recovered. The figure also points to increasing producer’ margins in both sectors along the bailout period.

Figure 2: Price

deflators and Unit Labour Costs (1995=100)

The second fact in the figure is that, until 2008, prices increased much faster in Services than in Manufactures. This is the textbook response to a large capital inflow, as manufactures are exposed to international competition while many sectors in services are basically not. The figure thus illustrates quite clearly why the increase in economy-wide unit labour costs in Portugal relative to other countries has little to do with dysfunctional wage setting: unit labour costs increased wherever prices increased. In this particular episode, the real exchange rate measured with unit labour costs captures basically the increase in the relative price of non tradable goods, not wage productivity gaps.

Figure 3 turns to nominal wages. To stick

with wages in euros (instead of using an index), we use a little trick: we

simulate the marginal product of labour, by multiplying the average product of

labour in nominal terms each year by the average share of labour in Gross Value

Added along 1995-2010, which we take as proxy for b (that is, we compare W

with bPV/L, presuming an unchanged b). The advantage of this procedure

is that it takes as reference the entire period, rather than a base year, so we

move forward, risking some measuring.

Figure 3: Nominal wages and the (simulated) marginal

product of labour (ECU/Euro)

As shown in the figure, nominal wages

increased in both sectors during the capital inflow episode. The stylized interpretation is that the

expansion in the demand for labour in non-tradable goods sectors caused wages

to increase in manufactures too. The fact that wages evolved almost

proportionally in manufactures and in services along most of the period is suggestive

of cross-sector labour mobility.

The figure also reveals that, during the bailout

period, nominal wages evolved in different directions in manufactures and in

services. To a large extent, this reflects the cuts in government sector wages.

Turning to the wage gaps, as shown in

Figure 3, departures of nominal wages away from the calibrated “labour demand”

remained small along most of the period until 2008. In the case of

manufactures, a significant positive wage gap emerged in 2009 (+4.6%).

This was subsequently replaced by a negative one, that reached -4.6% in 2012. In

the case of Services, gaps have also remained modest along most of the period, but

a significant -4.3% emerged in 2012. Note that the negative wage gap in services

cannot be accounted for by the cuts in public sector wages, because government

wages and productivity are the same.

Because the data on services above accounts

for many sectors, including the government, it is worth looking

inside. Unfortunately, detailed data by INE is available until 2011 only.

In order not to repeat the three steps above,

we focus on a summary variable, the labour share on gross value added, or –

which is the same – the ratio between real wages and productivity (s=WL/PV). Without

frictions, the labour share should be constant and equal to the elasticity of

labour in the production function, b. The difference between these two, s/b (or 1/Z),

is often labelled the “real wage gap”.

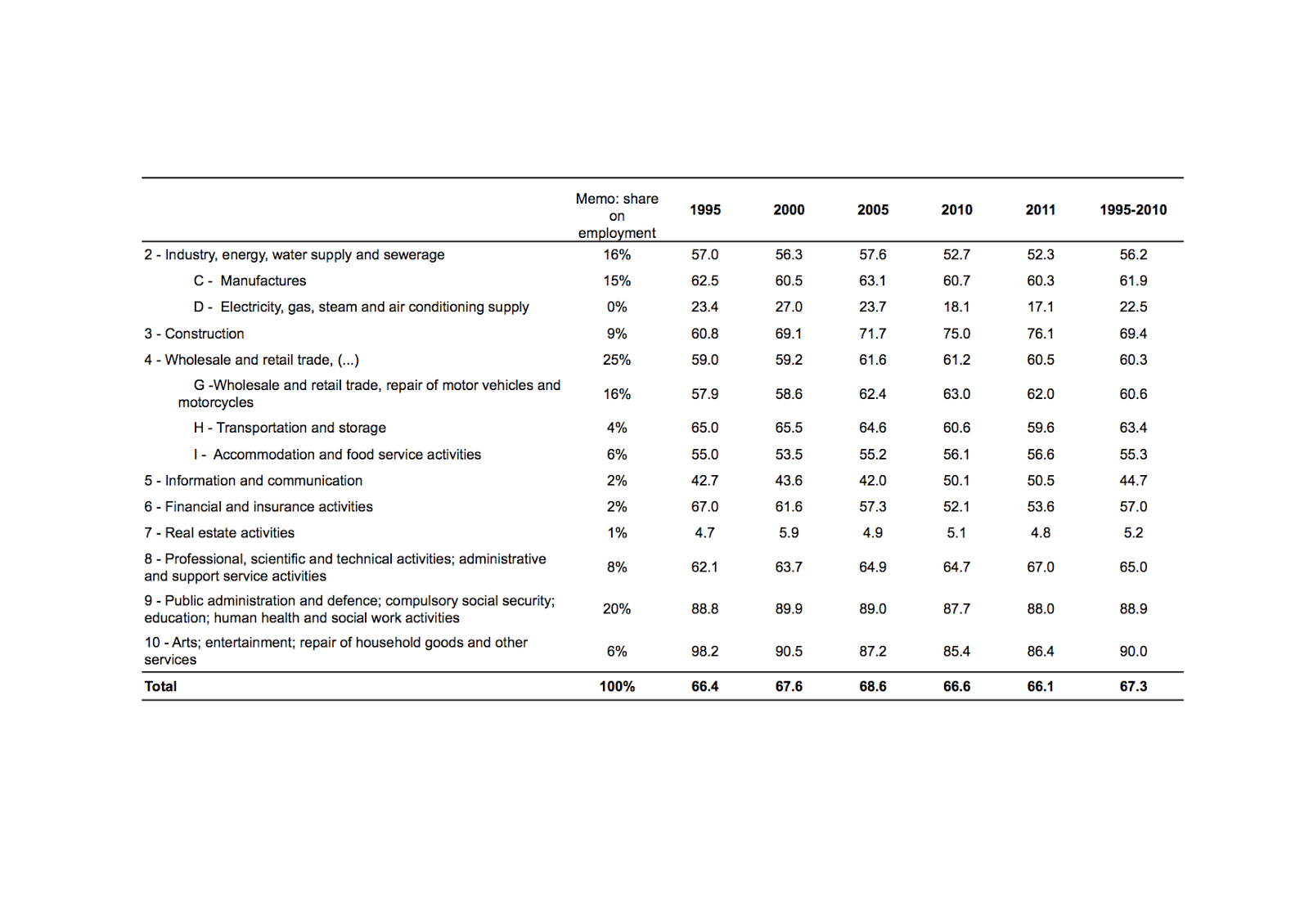

Table 1 displays the shares of labour in gross value added at the sectoral level (agriculture is excluded because the adjustment employment/employees produces odd results). The first column displays the shares on employment, as of 2010. The last column shows the average labour shares along 1995-2010.

As shown in the table, at the country level, the share of labour on domestic income has remained pretty stable around 67.3, reaching a maximum of 68.6 in 2005. With no question, this is too little to support the claim that wages have in general evolved ahead of productivity. In the case of manufactures in particular, the maximum observed labour share was 64.9 in 2009, which compares to the 61.9 average (hence, the +4.6% gap). In 2010, the gap in manufactures was already negative.

In general, labour shares at the sectoral level are more or less trendless. There are however, some exceptions: on the up-side, "information and communication" stands out ("Building and construction" too, but we have reasons to suspect that the data for this sector, as well as for agriculture, is plagued by changes in the proportion of temporary labour or by changes in the level of informality); on the downside, sectors where the wage

shares have been declining include "Transportation and storage", "Arts and entertainment" and – guess what

– energy supply. The industry of financial services also exhibited a declining labour share until 2008, but the productivity fall in the years that followed partially reverted the situation.

Table 1 – Labour shares

Summing up

1 – The claim that real wages have departed significantly above productivity does not match the national accounts data. In the case of manufactures, the maximum observed real wage gap amounted to 4.6%, during the 2009' collapse of international trade, to recover one year after.

2 – In general the data supports the

narrative that aggregate demand effects, rather than nominal wage stickiness explain the pre-2008

external imbalance: during the capital inflow episode, prices of non-tradable

goods increased, pressing nominal wages up. This forced average productivity in manufactures

to increase, in some cases with technological change, but mostly through the shutting down of low productivity firms, while labour was reallocated to

low-productivity-growth non-tradable good sectors.

3 – The preliminary data for the bailout episode

suggests that real wages have been evolving below productivity, not the other way

around. By 2011, this trend was more evident in transportation and storage, financial services, and energy supply.

4 – The preliminary data for 2012 also points

to the case that real wages in manufactures fell short the productivity trend

by some 4.6%. This suggests a scope for entrepreneurs to raise

profits by hiring more workers. However, there are reasons to believe that in

the current juncture, other factors apart from labour costs are constraining

the entrepreneurs’ choices. This will be the subject of my next post.