This is not the first time that the European integration construct faces challenges. Jump back in time to the 1992-1993 crisis of European exchange-rate mechanism (ERM). Members had experienced different path in unit labor costs (divergence), there had been a (very) large assymetric shock (Germany reunification), the European political project was perceived as weaker (French and Danish referendum) and European leaders unable to coordinate (Bath summit).

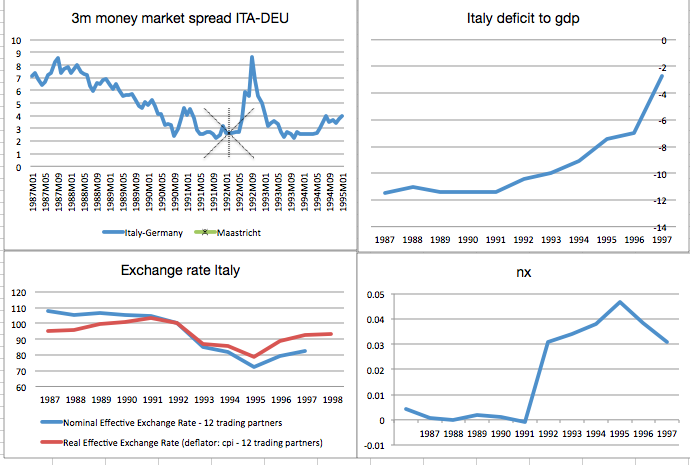

The next graphs show the case of Italy during the EMS crisis. I use this case to make two points.

The first is that Italy was ultimately able to adjust without external help thanks to, an ambitious fiscal consolidation, structural reforms and privatizations (circa 10% GDP). However in that case as in many others the forced devaluation of the Italian lira improved the trade balance and contributed significantly to the success of the adjustment.

The second is on coordination. The 13 years of ERM existence at the moment of the crisis had pushed members to design effective procedures to coordinate the setting of the exchange rate parities. In the best European tradition, the decision of setting central rates required unanimous approval. Unfortunately the “un pour tous, tous pour un” approach is designed for a group that stays loyal to each other through thick and thin. The latter is not the best description of European leaders during the EMS crisis when realignment became “a dirty word in Bath.” In absence of multilateral consensus, Italy and Germany had to bilaterally propose that the Lira would devalue by 3.5% and the Mark revalue by 3.5% against all currencies in the ERM. Some members refused. The lira was initially the only currency to be devalued (by 7%). Ultimately the lira took a leave from the ERM to reenter a few years later with a currency devalued by 30%.

Today the absence of a nominal devaluation implies that the adjustments are more difficult. The number of national policies that can emulate the effects of a devaluation and help the adjustment of external imbalances is reduced.

A possibility is to use neutral tax swaps. In a recent work I have looked to the effects of a “fiscal devaluation,” namely a decrease in labor taxes balanced by an increase in consumption taxes. It is not a perfect substitute of a nominal devaluation: it has advantages, such as no adverse effect from foreign denominated debt (different situation from 1992), and has disadvantages, such as the difficulty to implement it compared to a currency devaluation. Nevertheless, it is a policy that aims at reducing external imbalances within a currency area. The existence of policies that can achieve a devaluation or a revaluation (do the opposite: decrease consumption tax, increase labor tax) within the currency area suggests that such policies require coordination between members. Here the lessons learned during the ERM period can prove useful. During the ERM, in front of imbalances, European finance ministers were changing parities between exchange rates. During the EMU, in front of imbalances, European finance ministers could change the composition of their tax rates. In the “un pour tous, tous pour un” world this would imply that EMU members with large and persistent trade deficits should fiscally devalue, while members with large and persistent trade surpluses should fiscally revalue.

Another possibility would be to increase the fiscal integration of the union and allow for implicit or explicit fiscal transfers between members (many good proposals have been advanced). Realistically it is a medium run perspective. Monetary union required decades, fiscal union will not be made in a week nor in a year.

We have experienced that in our journey towards European economic integration and convergence, imbalances continue to appear. Now we need these imbalances to be controlled using policy instruments that are coherent with the degree of national sovereignty determined by political constraints. Ultimately we need to accept that these imbalances matter.

May I just add that I believe a sharp reduction in labour taxes could potentially greatly benefit those with low skills who are out of a job as the current floor of minimum wage plus labour taxes makes it too expensive to employ them. The problem is whether the current social security benefits system creates a disincentive for them to work...

ReplyDelete